1h 30 min

Introduction to Real Estate Financing

Welcome to one of the most critical areas of real estate: how people actually afford to buy property, and how taxes come into play. Real estate isn’t just about choosing the right home—it’s about understanding how the numbers work behind the scenes.

Real estate financing plays a crucial role in facilitating property purchases and real estate investments. The majority of buyers depend on financing solutions to fill the financial gap between their available funds and the property's total cost. By spreading the property's expense over an extended period, financing renders home ownership attainable and manageable for a wide range of individuals.

Why is financing in Real Estate transactions important?

Financing a property unlocks opportunities in several powerful

Affordability - Financing makes expensive real estate transactions manageable with affordable monthly payments over time.

Increases Buying Power - Financing enables buyers to access larger loans, expanding their property options beyond their immediate means.

Investment Opportunities - Real estate financing lets investors leverage capital and acquire multiple properties, potentially increasing ROI.

Home ownership - For most individuals and families, owning a home is a significant life goal. Real estate financing makes this dream achievable by spreading the cost over time.

Tax Benefits - In some cases, mortgage interest payments and property taxes may be tax-deductible, providing potential financial advantages to homeowners.

This is why understanding financing options isn’t just useful—it’s essential.

Common Financing Options

There are many different options for financing a real estate property and these are the main ones that you should know:

Cash (self financing): Self-financing means using personal funds to purchase a property without external loans. No mortgage process is involved, providing a faster transaction with no interest payments, but it ties up a significant portion of the buyer's capital.

Conventional Mortgages: These are standard home loans offered by banks and traditional lenders, typically requiring a down payment and offering varying loan terms and interest rates.

Buy-to-Let Mortgages: Investors can opt for buy-to-let mortgages to finance properties intended for rental purposes, with specialized terms and interest rates.

Shared Ownership: This option allows buyers to purchase a share of a property and pay rent on the remaining portion, often helping first-time buyers enter the market.

If you’re guiding clients or planning your own purchase, knowing which type fits their goals is key.

What is a mortgage?

A mortgage is a loan from a bank or lender to help you buy a home. You repay it in monthly installments, including interest, over an agreed period. If payments aren't made, the lender can take back the property. Typically interest rates on secured loans will be lower than on unsecured loans but will be riskier as if the buyer fails to keep up with their payments their home would be repossessed by their lender.

There are a few common types of mortgages:

Fixed rate mortgages

A fixed-rate mortgage provides stable, predictable monthly payments, shielded from Bank of England rate changes. However, it doesn't offer benefits from rate decreases, and after the fixed term, it may switch to a costlier standard variable rate if a new deal isn't secured.

Standard Variable Rate mortgages (SVR)

A variable rate mortgage means fluctuating monthly payments as the interest rate - decided by the lender - can change. After the introductory deal, borrowers are often switched to a costlier Standard Variable Rate (SVR). To avoid higher costs, it's advisable to switch to a new deal.

Tracker mortgages

A tracker mortgage follows the Bank of England base rate, plus an additional percentage, leading to variable monthly payments. Rate adjustments usually occur the month after base rate changes. Some tracker deals have a minimum rate safeguard, preventing the rate from dropping below a specific level, even if the base rate falls further.

Fixed Mortgage

Advantages:

Interest rate remains stable for a fixed period, ensuring predictable monthly payments.

Offers protection against rising interest rates during the fixed term.

Easier budgeting thanks to consistent payment amounts.

Disadvantages:

Initial interest rates are typically higher than variable options.

Penalties may apply for early repayment or switching before the term ends.

Limited flexibility if interest rates drop significantly; remortgaging could be challenging after the fixed period.

Variable Mortgage

Advantages:

Typically starts with a lower interest rate, which can save money early on.

If interest rates drop, monthly payments may decrease.

More flexibility in making extra payments or paying off the mortgage early, often without penalty charges.

Disadvantages:

Monthly payments can increase unpredictably if interest rates rise.

Budgeting is more difficult due to fluctuating monthly costs.

Significant rate hikes can lead to financial strain or the need to switch to a fixed rate.

Each option comes with trade-offs depending on whether you want stability or flexibility.

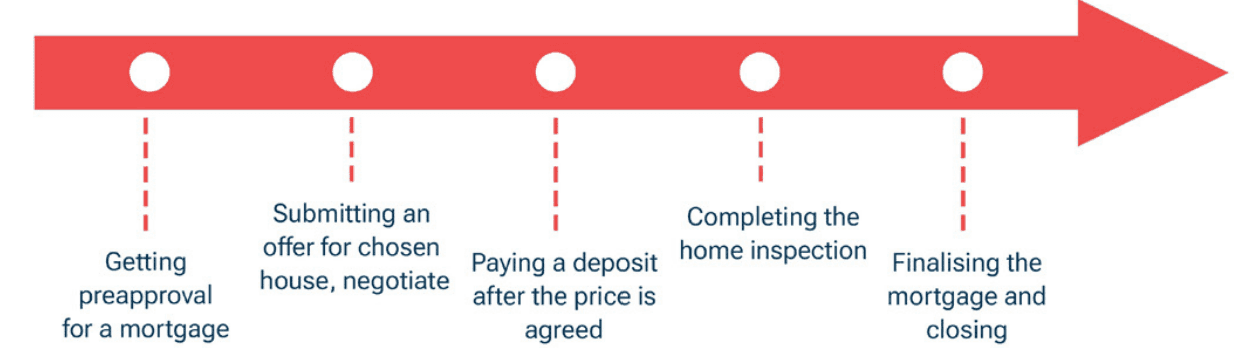

How will a mortgage work?

Key requirements for a mortgage approval

Before you can get a mortgage, lenders will look at three main factors:

Positive credit history: 620-999 credit score to get approved for a mortgage with increasingly good offers.

Steady income: The qualified amount to borrow is typically 4-4.5 times the household income.

Low debt levels: Lenders generally favour a debt-to-income ratio below 36%.

The Deposit, the LTV ratio and PMI

To purchase a property with a mortgage, borrowers need a deposit of at least 5% of the property's value, with the average being around 10%-20%.

The deposit size affects the loan-to-value (LTV) ratio.

LTV is the mortgage amount divided by the property value.

Mortgage amortisation

Mortgage amortization is the gradual repayment of a loan through regular monthly payments, which covers both interest and the initial loan amount (principal). The balance reduces over time until the loan is fully repaid by the end of the term.

Types of repayment

There are two main ways to repay a mortgage:

Interest-only mortgages require the borrower to make monthly payments that solely cover the interest on the borrowed amount. The full repayment of the mortgage is deferred until the mortgage term reaches its conclusion.

Repayment mortgage is where the borrower pays back capital and interest at the same time.

Some investors prefer interest-only for short-term flexibility, while most homeowners go for repayment to gradually own their home.

Early repayment & exit

Things change. And your mortgage can too.

Remortgaging: As a mortgage term concludes, they can switch to a new deal with their current lender or a new one, providing better rates, terms, or accessing equity.

Overpayment: Making additional payments beyond the required amount on certain mortgages can accelerate repayment and potentially reduce interest costs.

Selling the Property: Exiting the mortgage by selling the property allows them to use the proceeds from the sale to repay the outstanding mortgage balance.

These options provide flexibility as your financial situation evolves.

Types of borrowers

Understanding buyer profiles helps tailor advice:

First time buyer: A person who has never had a mortgage before.

Home-owner: A person who owns his/her own home either with or without a mortgage.

Re-mortgagor: A person who owns a property with a mortgage and is looking to refinance.

Large loan borrower: A person who is looking for a mortgage in excess of £500k.

Each group faces different requirements and benefits.

Buy-to-Let

What is a buy-to-let mortgage?

Buy-to-let (BTL) mortgages cater specifically to landlords interested in purchasing a property with the intention of renting it out. These mortgages are subject to distinct regulations compared to standard residential mortgages.

Who is eligible for a Buy-to-Let mortgage?

Lenders will have different criteria for whom they are willing to give a buy-to-let mortgage as they are considered a higher risk. The criteria will vary between different lenders and they may include the following.

It may be required that they already own their own home, either outright or with an existing mortgage.

They should certainly have a fairly high credit score and little to no debt tied up elsewhere.

They may be asked to present proof of employment income or earnings from self-employment, apart from rental earnings. For most lenders they have to be earning £25,000+ before applying for a buy-to-let.

There is a maximum age requirement of 75 years old and some lenders could set it lower.

A minimum of a 25% deposit would have to be provided for a buy-to-let mortgage, this is typically going to be higher than standard residential mortgages.

The rental income that would be received from the property has to at least be covering 125% of their mortgage repayments or in some cases up to 145%.

Key differences of buy-to-let mortgages

Interest rates will usually be higher and overall costs will also be greater compared to ordinary mortgages.

Most buy-to-let mortgages are typically interest-only, meaning they pay the interest each month but not the actual capital amount for the property. Then when the mortgage term ends the original loan will have to be paid with a lump sum fully.

Some buy-to-let mortgages are also available as a repayment mortgage.

Lenders usually require a higher deposit (lower LTV ratio) for buy-to-let properties, often around 25% to 40% of the property's value.

ONLY FOR OVERSEAS BUYERS:

If you are an overseas buyer who wants to buy a property in the UK, you may be able to get a loan from some lenders. However, you should be aware that you will need to pay a higher deposit, usually 20-30% of the property value.

Your loan eligibility will depend on various factors, such as your credit history, your income level, and even country of your residence. We can connect you with a broker who can answer your questions and find the best option for you.

One advantage of buying an off-plan property is that you don't need to show any mortgage approval at the time of reservation. You only need to pay 10% of the deposit and the rest will be due upon completion, whether you pay by cash or loan.

Shared Ownership & First Home Scheme

To support affordability, the UK offers two key buying schemes:

SHARED OWNERSHIP

What is a shared ownership mortgage?

Shared ownership is a government-backed scheme that allows you to buy a percentage of a property (usually 25-75%) and pay rent on the remaining share. Over time, you can increase your ownership through a process called "staircasing." This option makes home-ownership more affordable, especially for first-time buyers.

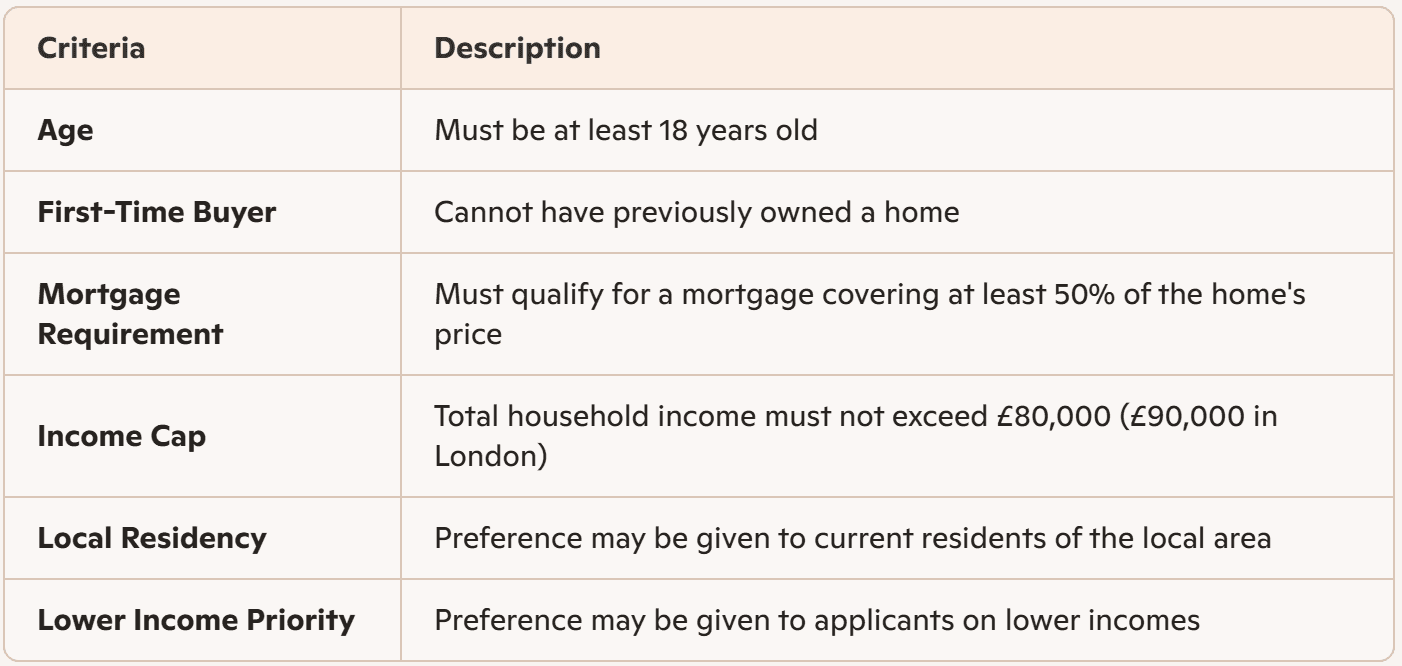

Who is eligible for a shared ownership mortgage?

Shared ownership schemes are only available to permanent UK residents who have to meet some of the following categories.

Have a household income below £80,000 (or below £90,000 if based in London)

Be a first-time buyer

Currently live in a shared ownership property

Be a former homeowner unable to afford to buy again

Be currently renting from a council or housing association

How will a shared ownership mortgage work?

Shared ownership schemes operate by enabling the buyer to secure a mortgage for a portion of the property while covering the rest through rental payments. This arrangement can potentially allow them to purchase a home with a reduced deposit requirement. When purchasing a home through shared ownership, they would usually buy a share between 10%-75%.

Example:

They buy a 50% share in a house worth £300,000, which is £150,000.

If they put down a 5% deposit of £15,000 on that share of £150,000. They'll then have a mortgage of £135,000.

They'll then rent the rest of the property from the housing association.

Their total monthly payments will combine their rent and mortgage repayments.

Before being approved for a shared ownership scheme some details would need to be provided such as the household income and credit history, and ultimately, the amount a buyer would be able to borrow would depend on the income, cost of mortgage, rent, service charges and ground rent.

More shares can be bought after the initial purchase- known as staircasing- up to the full 100% ownership.

All shared ownership homes will be a leasehold property so the buyer would only own the property and not the land it's built on.

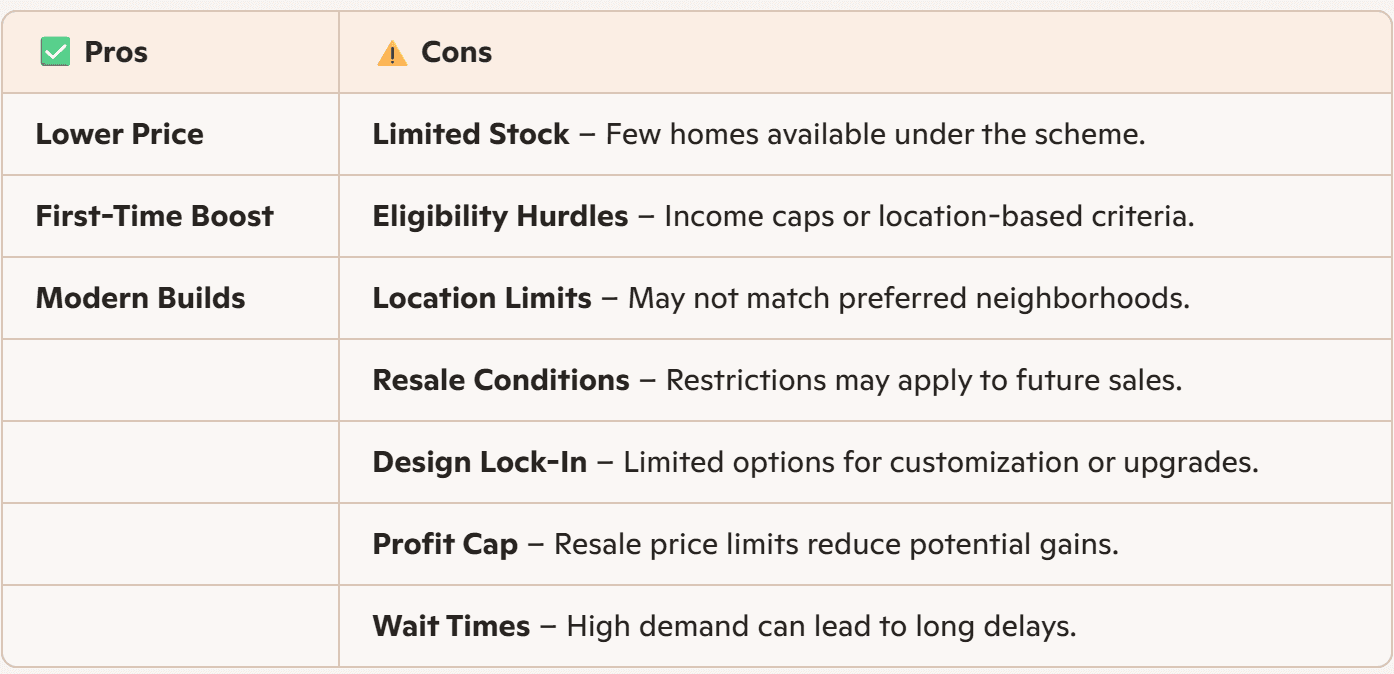

Pros

Affordability: Lower deposit and monthly mortgage payments compared to purchasing the property outright.

Staircasing: Opportunity to increase ownership share over time and reduce rent payments.

Easier Entry: Ideal for first-time buyers and those needing help to afford a property.

Cons

Limited Control: Co-ownership may mean limited decision-making power for property changes, requiring agreement from other owners.

Rent Payments: Rent on the portion not owned adds to monthly costs and may increase over time.

Leasehold Obligations: Leasehold properties come with ongoing obligations such as ground rent and service charge.

Staircasing Costs: Increasing ownership share through staircasing involves additional expenses like valuation and legal fees.

Selling Difficulties: Selling shared ownership properties can be more complex, requiring approval from the housing association.

Limited Investment Potential: Shared ownership property resale values may not appreciate as quickly as traditional properties.

Shared Responsibilities: Co-owners share maintenance, repairs, and decisions, which lead to disagreements.

FIRST HOME SCHEME

What is the first home scheme?

The First Homes Scheme is a government initiative that helps first-time buyers purchase a home at a discounted price, usually 30-50% off the market value. It is designed to make home-ownership more affordable for local buyers and key workers.

Who is eligible for the First Home Scheme?

The first home scheme is only available in England to those who are eligible and meet the following criteria.

Who could be prioritised for the First Home Scheme?

The local council may also set some eligibility conditions to whom they priorities approving for the scheme.

How will the first home work?

The first home scheme works much like a regular mortgage but buyers have to get a significantly cheaper mortgage.

A key difference however is that if an owner of a property purchased through the first home scheme decides to sell their property there are restrictions.

The property must be sold to a buyer who themselves qualify for the first home scheme.

The same percentage discount must be applied to the current value of the property as what it was originally purchased with.

These options help bridge the gap for buyers who need extra support entering the market.

Next Steps Before Exploring Real Estate Taxation

Now that we've unpacked how property financing works—covering mortgages, buyer profiles, and repayment strategies—you should have a solid grasp of how buyers afford real estate and what options they have depending on their goals.

With financing in place, the next important topic is taxation. Understanding the costs that come with purchasing, owning, renting, and selling property helps clients plan smarter and avoid surprises.

Let’s take a look at how UK property taxes work and what every buyer or investor needs to know.